Question 1

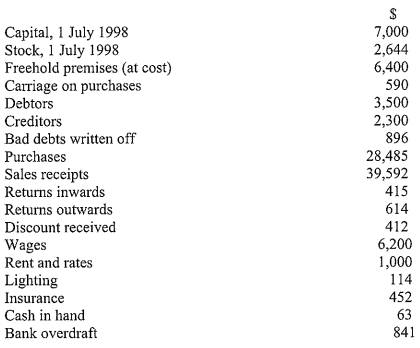

Lin has been in business as a retailer and the following balances were extracted from his books on 31 December 1998.

You are required to prepare the Trading, Profit, and Loss Accounts for the half year ended 31 December 1998 and a Balance Sheet as of that date showing as much detail as possible and taking into account the following:

- The closing stock was valued at $2,089;

- Lin had withdrawn for his own personal use, $100 from the sales receipts every month. This has not been taken into account;

- A provision of 5% of debtors is to be created;

- of the $452 for insurance, $68 was the insurance premium for Lin’s own private dwelling; (v) It was estimated that $37 was owed for lighting.